Shopping for business equipment is easier when you know what financing options may be available before you start negotiating. That is why it helps to learn how to get prequalified for equipment financing early.

Many business owners find the machine, truck, trailer, or equipment package first and then try to figure out financing afterward. That can work, but it can also create delays, uncertainty, and pressure if the seller wants a quick decision.

Getting prequalified before shopping can help you understand your options earlier in the process. It may give you a better idea of possible approval range, payment structure, documentation needs, and whether your business profile is likely to fit available equipment financing programs.

Prequalification is not the same as final approval, but it can be a useful first step before you commit to a purchase.

What Does It Mean to Get Prequalified for Equipment Financing?

Equipment financing prequalification is an initial review of your business, credit profile, equipment needs, and financing request.

The goal is to estimate whether financing may be available and what general options may fit before a final lender approval is issued.

A prequalification may review information such as:

- Business name and contact information

- Time in business

- Industry

- Estimated equipment cost

- Equipment type

- Credit profile

- Revenue or bank statement information, if needed

- Whether the equipment is new or used

- Whether the seller is a dealer, vendor, auction, or private party

A final approval may still require additional documentation, lender review, equipment details, seller verification, and completed financing documents. Still, prequalification can help you avoid shopping blind.

Why Get Prequalified Before Shopping?

Getting prequalified before shopping for equipment can save time and help business owners make better decisions.

Instead of guessing what you can afford or waiting until the last minute, you can shop with a clearer understanding of your possible financing path.

Prequalification may help you:

- Understand a realistic equipment budget

- Compare monthly payment options before buying

- Avoid wasting time on equipment that does not fit your financing profile

- Move faster when you find the right machine or asset

- Negotiate with more confidence

- Prepare documents before the seller needs them

- Compare paying cash versus financing

- Preserve working capital for operations and growth

For many business owners, the benefit is not just getting financing. The benefit is knowing what options may be possible before the purchase decision becomes urgent.

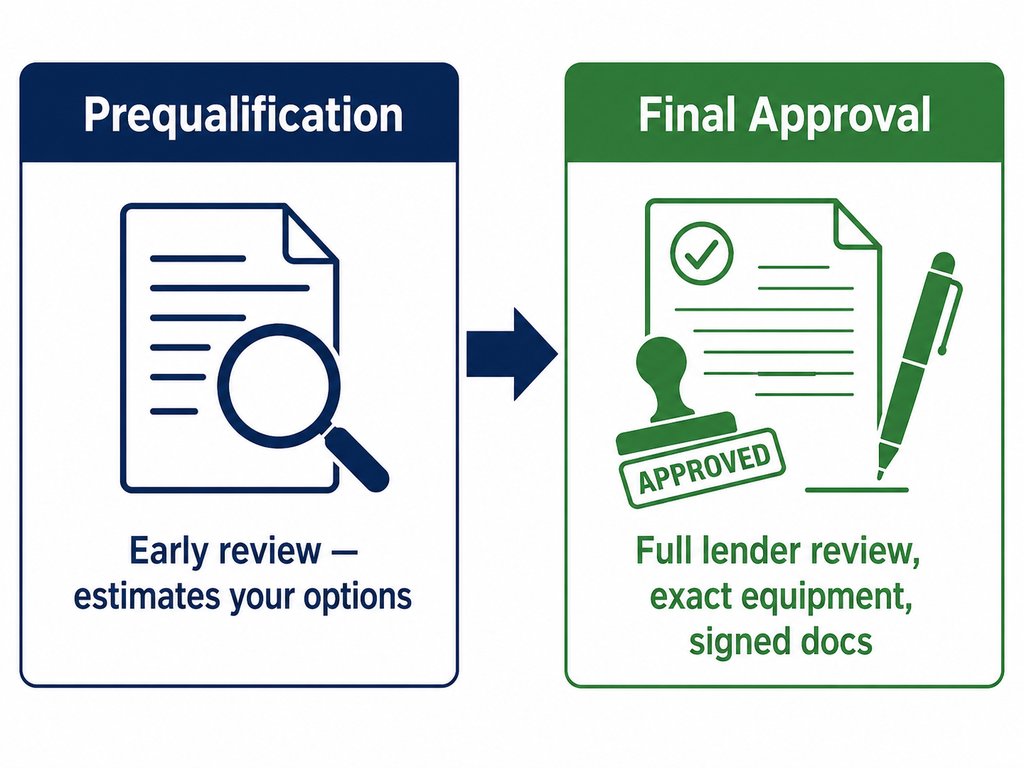

Prequalification vs. Final Approval

It is important to understand the difference between prequalification and final approval.

Prequalification is usually an early review based on the information provided. It may help identify possible options, but it is not a guarantee of financing.

Final approval typically happens after a lender reviews the complete application, supporting documents, equipment details, seller information, and any required verification.

For example, a business may be prequalified based on credit, time in business, and estimated equipment cost. Final approval may still depend on the exact equipment, invoice, seller, title or serial number, lender underwriting, and signed documents.

That is why business owners should treat prequalification as a helpful planning step, not a completed funding commitment.

Step 1: Know What Type of Equipment You Need

Before applying for prequalification, it helps to know the general type of equipment you plan to buy.

You do not always need the final invoice right away, but you should have a clear idea of the equipment category, estimated price, and business purpose. Examples include:

- Skid steer for a construction company

- Box truck for a delivery business

- Commercial oven for a restaurant

- CNC machine for a manufacturing shop

- Dental equipment for a practice

- Trailer and mower package for a landscaping business

- Commercial drone package for surveying, agriculture, or inspection work

The more specific you can be, the easier it may be to match the request to the right financing option.

Step 2: Estimate the Equipment Cost

You should have a realistic estimate of the equipment cost before starting the prequalification process. This can come from:

- Dealer quote

- Vendor proposal

- Auction listing

- Private seller asking price

- Manufacturer quote

- Online listing

- Budget range based on comparable equipment

The cost matters because financing options can vary by amount. A $15,000 equipment request may be reviewed differently than a $150,000 request. A lower-cost tool package may require a different structure than a high-value machine, truck, or medical device.

If you are not sure of the exact cost yet, start with a realistic range. You can update the request once you find the specific equipment.

Step 3: Review Your Time in Business

Time in business is one of the common factors lenders may review when evaluating equipment financing.

Established businesses may have more financing options because they can show operating history. Newer businesses and startups may still qualify, but requirements are often stronger and may depend more heavily on credit profile, industry, equipment type, down payment, collateral, or other factors.

Business owners should be ready to provide the date the business started and, if relevant, whether prior industry experience or prior sole proprietor history applies.

Step 4: Understand Your Credit Profile

Credit profile may affect available financing options, approval terms, down payment requirements, and documentation needs.

For equipment financing, lenders may review personal credit, business credit, or both depending on the program and business structure.

A stronger credit profile may create more options. A weaker credit profile does not always mean financing is impossible, but it may affect the type of program, cost, structure, down payment, or documentation requested.

The best approach is to be realistic upfront. Trying to hide credit issues usually creates delays later. If there has been a bankruptcy, repossession, late payments, or other credit challenge, it is better to know whether alternative structures may be available early in the process.

Step 5: Gather Basic Business Information

Prequalification usually starts with basic business information. You may not need every document at the first step, but having the basics ready can help the process move faster.

Common information may include:

- Legal business name

- Business address

- Business phone number and email

- Entity type

- Industry

- Time in business

- Owner information

- Estimated annual or monthly revenue

- Equipment type and estimated cost

- Seller or vendor information, if known

Depending on the amount, program, and lender, additional documentation may be requested later.

Step 6: Prepare Equipment Details

The equipment itself matters. Lenders may want to understand what the equipment is, how it will be used, and whether it has value as a business asset.

Helpful equipment details may include:

- Year, make, and model

- Serial number or VIN, if available

- New or used condition

- Purchase price

- Seller name and contact information

- Invoice, quote, or bill of sale

- Auction listing, if applicable

- Equipment location

- Any attachments, software, delivery, installation, or training costs

You may not have all of this information at the prequalification stage, but you will usually need more detail before final approval and funding.

Step 7: Consider the Seller Type

Where you buy the equipment can affect the financing process.

Buying from a dealer or vendor may be more straightforward because the seller can usually provide a formal quote or invoice. Auction and private party purchases may still be possible, but they can require additional verification.

Seller types may include:

- Equipment dealer

- Manufacturer or vendor

- Private seller

- Auction company

- Online marketplace

- Another business selling used equipment

If you plan to buy from a private seller or auction, getting prequalified before making an offer or bidding is especially important. It can help you understand what may be required before money needs to move quickly.

Step 8: Compare Monthly Payment to Cash Purchase

Prequalification can help you compare the impact of financing versus paying cash.

The goal is not only to ask, “Can I afford this equipment?” The better question is, “What happens to my cash flow after I buy it?”

Financing may help preserve cash for:

- Payroll

- Fuel

- Inventory

- Materials

- Rent

- Insurance

- Repairs

- Marketing

- Slow-paying customers

- Upcoming jobs or growth opportunities

If the equipment will help generate revenue, reduce downtime, or increase capacity, a monthly payment may be easier to manage than a large upfront cash purchase.

Step 9: Avoid Common Prequalification Mistakes

Business owners can improve the process by avoiding a few common mistakes:

- Waiting until the seller needs payment immediately

- Shopping without a realistic equipment budget

- Providing incomplete business information

- Using an estimated price that is far below the actual equipment cost

- Not mentioning that the equipment is used, auction, or private party

- Assuming prequalification is the same as final approval

- Ignoring cash flow and only focusing on whether a payment sounds affordable

- Failing to ask whether delivery, installation, software, or attachments can be included

The cleaner and more accurate the information is upfront, the easier it is to identify a financing path that may fit.

Step 10: Get Prequalified Before You Commit

The best time to get prequalified is before you sign a purchase agreement, place a large deposit, or bid aggressively at auction.

Prequalification gives you a better starting point. You can shop with more confidence, compare options, and avoid putting pressure on your business cash reserves without understanding the alternatives.

This is especially useful when equipment availability is limited or when a seller expects a fast decision.

What Happens After Prequalification?

After prequalification, the next steps usually depend on the lender, equipment, seller, and requested structure. The process may include:

- Selecting the specific equipment

- Submitting a quote, invoice, auction listing, or bill of sale

- Providing additional business or financial documents if requested

- Completing lender review and final approval

- Reviewing terms and payment structure

- Signing financing documents

- Completing any verification steps

- Funding the seller or vendor after requirements are satisfied

Exact steps can vary. Some transactions are simple, while others require more documentation because of the amount, seller type, equipment type, credit profile, or lender requirements.

Final Takeaway

Getting prequalified before shopping for equipment can help business owners make better purchase decisions.

Instead of finding equipment first and scrambling for financing later, prequalification gives you a clearer view of possible options before you commit.

It can help you understand your budget, compare monthly payments, preserve cash reserves, prepare documentation, and move faster when you find the right equipment.

Prequalification is not a final approval or guarantee of financing, but it is a smart first step for business owners who want to shop with more confidence.

Before you buy, compare the cost of using cash against the benefits of financing. The right structure can help your business get the equipment it needs while keeping working capital available for operations and growth.

Frequently Asked Questions About Equipment Financing Prequalification

Getting prequalified means your business information, credit profile, estimated equipment cost, and financing request are reviewed at an early stage to identify possible financing options. It is not the same as final approval or a guarantee of funding.

Yes, it can be helpful to get prequalified before shopping. Prequalification may help you understand your budget, compare monthly payment options, prepare documents, and move faster when you find the right equipment.

No. Prequalification is an initial review. Final approval usually requires complete lender review, equipment details, seller information, any requested documentation, and signed financing documents.

Common information may include business name, time in business, industry, owner information, estimated revenue, credit profile, equipment type, estimated equipment cost, and seller information if available.

In many cases, you can start with an estimated equipment type and price range. Final approval will usually require the exact equipment, invoice, seller details, and any lender-required documentation.

Some startups may be able to get prequalified, but requirements are usually stronger for newer businesses. Credit profile, down payment, equipment type, industry, and business plan may all matter.

The credit process can vary by provider and lender. Business owners should ask whether the initial review uses a soft pull, hard pull, or other credit review method before applying.

Yes, used equipment may be considered for financing depending on the equipment type, age, condition, seller, purchase price, business profile, and lender approval.

Ready to Get Prequalified?

BNC Finance helps business owners explore equipment financing options for new and used equipment across many industries.

Get prequalified before you shop so you can compare options before using your cash.

All financing is subject to credit approval. Prequalification is not a guarantee of approval, rate, term, structure, or funding. Terms, structures, rates, documentation requirements, down payment requirements, credit review methods, and availability vary by business profile, equipment type, seller, lender requirements, and approval. BNC Finance is not providing tax, legal, accounting, or financial advice through this article. Business owners should consult their own advisors before making financing, tax, legal, or business decisions.